Example usage

Here we demonstrate how to use scmrelax package to construct the counterfactual of the treated unit using relaxed balancing estimators.

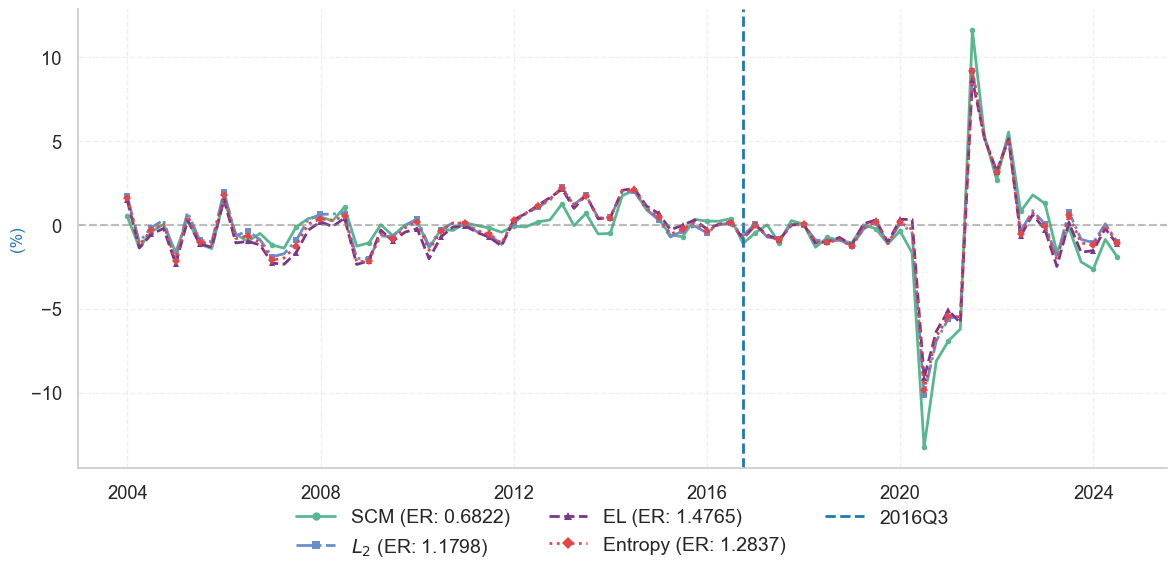

we examine the impact of the 2016 Brexit referendum on the United Kingdom’s GDP. On June 23, 2016, a referendum on the UK’s membership in the European Union resulted in 51.89% of voters favoring departure, triggering a withdrawal process that concluded on January 31, 2020. The referendum’s outcome was largely unexpected by markets. It prompts us to designate the third quarter of 2016 as the starting point for analyzing its effects.

We estimate the combination weights using YOY growth rate of quarterly GDP by 1. synthetic control (SCM), 2. EL-SCM-relaxation, 3. Entropy-SCM-relaxation, 4. L2-SCM-relaxtion. Then we use the esimated weights to construct the counterfactual GDP growth rate.

Setup and imports

import scmrelax

print(scmrelax.__version__)

0.1.0

import numpy as np

import matplotlib.pyplot as plt

import seaborn as sns

import warnings

import pandas as pd

# Set plotting style

plt.style.use('seaborn-v0_8-paper')

sns.set_style("whitegrid")

sns.set_context("notebook", font_scale=1.2)

# Suppress warnings

warnings.filterwarnings("ignore")

Data preprocessing

The processed_GDP.csv can be found in the folder.

# Read the preprocessed data

GDP = pd.read_csv('balanced_GDP_data.csv', index_col=0, parse_dates=True)

# Calculate GDP growth rate

GDP_growth = 100*GDP.pct_change(4).dropna()

# Define the function to prepare the data

def prepare_data(GDP_growth, target_country, pre_treat_date):

"""Prepare data for synthetic control analysis."""

y = GDP_growth[target_country]

X = GDP_growth.drop(target_country, axis=1)

y_pre = y.loc[:pre_treat_date]

X_pre = X.loc[:pre_treat_date]

country_list = X_pre.columns

return (y.to_numpy(), X.to_numpy(),

y_pre.to_numpy(), X_pre.to_numpy(),

country_list)

# Prepare data for analysis

target_country = 'United Kingdom'

pre_treat_q = '2016-06-30'

treat_q = '2016-09-30'

y, X, y_pre, X_pre, country_list = prepare_data(

GDP_growth, target_country, pre_treat_q

)

# print the sample size and the size of the donor pool

print("(Pre-treatment periods, Donor pool size): ", X_pre.shape)

(Pre-treatment periods, Donor pool size): (51, 57)

Estimate the weights and construct the counterfactual growth rates

Note: The following code requires a valid MOSEK license. Without a license, the code will raise an error.

results = scmrelax.fit(X_pre, y_pre, X)

Evaluate the in-sample empirical risks

# Calculate in-sample error rates

treatment_time = y_pre.shape[0]

ER_scm = np.mean((results['scm']['predictions'][:treatment_time] - y_pre)**2)

ER_EL = np.mean((results['EL']['predictions'][:treatment_time] - y_pre)**2)

ER_entropy = np.mean((results['entropy']['predictions'][:treatment_time] - y_pre)**2)

ER_l2 = np.mean((results['l2']['predictions'][:treatment_time] - y_pre)**2)

print("In-sample Empirical Risks:")

print(f"SCM: {ER_scm:.4f}")

print(f"EL-SCM-Relaxation: {ER_EL:.4f}")

print(f"Entropy-SCM-Relaxation: {ER_entropy:.4f}")

print(f"L2-SCM-Relaxation: {ER_l2:.4f}")

In-sample Empirical Risks:

SCM: 0.6822

EL-SCM-Relaxation: 1.4765

Entropy-SCM-Relaxation: 1.2837

L2-SCM-Relaxation: 1.1798

Plot the gap between realized growth rate and fitted growth rate

# define some colors

color_SCM = '#59B78F'

color_L2 = '#6A8EC9'

color_EL = '#7A378A'

color_entropy = '#E84446'

color_real = '#1f77b4'

color_treatment = '#1f77b4'

# Convert to time series

y = pd.Series(y, index=GDP_growth.index)

y_fit_scm = pd.Series(results['scm']['predictions'], index=GDP_growth.index)

y_fit_EL = pd.Series(results['EL']['predictions'], index=GDP_growth.index)

y_fit_entropy = pd.Series(results['entropy']['predictions'], index=GDP_growth.index)

y_fit_l2 = pd.Series(results['l2']['predictions'], index=GDP_growth.index)

# Create figure with style guide settings

plt.figure(figsize=(12, 6))

# Plot all differences with enhanced distinction

# SCM: solid line with markers

plt.plot(y-y_fit_scm, color=color_SCM, label=f'SCM (ER: {round(ER_scm, 4)})',

linewidth=2, linestyle='-', marker='o', markersize=4, markevery=2)

# L2: dash-dot line with squares

plt.plot(y-y_fit_l2, color=color_L2, label=f'$L_2$ (ER: {round(ER_l2, 4)})',

linewidth=2, linestyle='-.', marker='s', markersize=4, markevery=2)

# EL: dashed line with triangles

plt.plot(y-y_fit_EL, color=color_EL, label=f'EL (ER: {round(ER_EL, 4)})',

linewidth=2, linestyle='--', marker='^', markersize=4, markevery=2)

# Entropy: dotted line with diamonds

plt.plot(y-y_fit_entropy, color=color_entropy, label=f'Entropy (ER: {round(ER_entropy, 4)})',

linewidth=2, linestyle=':', marker='D', markersize=4, markevery=2)

# Add y-axis label

plt.ylabel('(%)', fontsize=12, color = '#1f77b4')

# Add treatment line

treatment_date = GDP_growth.index[treatment_time]

plt.axvline(x=treatment_date, color=color_treatment, linestyle='--', label='2016Q3', linewidth=2)

# Add zero line

plt.axhline(y=0, color='grey', linestyle='--', alpha=0.5)

# Add legend with enhanced visibility

plt.legend(

loc='upper center',

bbox_to_anchor=(0.5, -0.05),

ncol=3,

fontsize=14,

frameon=True,

facecolor='white',

edgecolor='none',

markerscale=1.5 # Make markers larger in legend

)

# Add grid with reduced opacity

plt.grid(True, linestyle='--', alpha=0.3)

# Remove top and right spines

plt.gca().spines['top'].set_visible(False)

plt.gca().spines['right'].set_visible(False)

# Adjust layout

plt.tight_layout()

plt.show()